- Certified phone accessories store

- 0616818330

- info@fulloriginal.nl

After you sign up for a keen FHA loan otherwise pre-approval and just have refused, it may be discouraging

Bonusy Demon Jack 27 automat wyjąwszy depozytu po kasynie przez internet 2024

January 29, 2025Noppes gokkasten performen gokkasten meerdere 19 betaallijnen buitenshuis aanmelden

January 29, 2025Understand the loan processes with the aid of are not expected concerns plus the answers from financial professionals. Select our directory of groups to see Faqs to suit your specific area of interest.

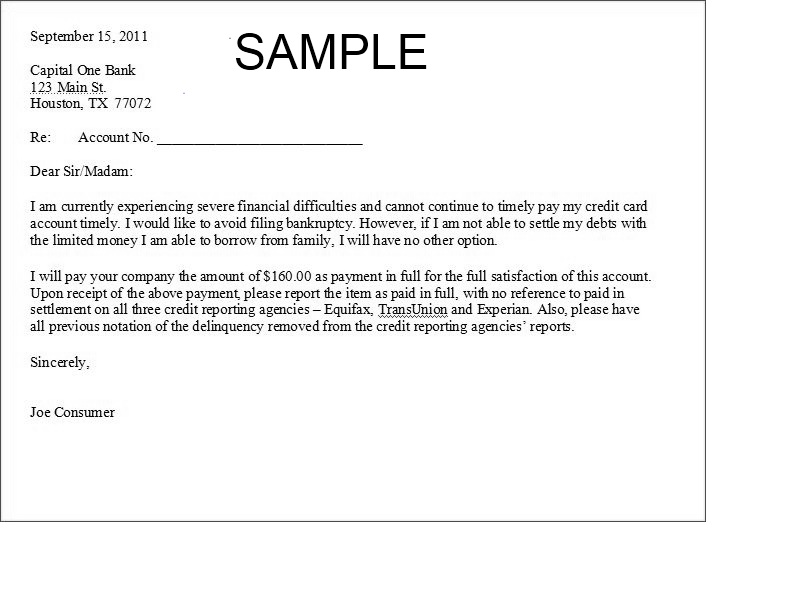

In the event that anything looks in your credit report that you like in order to challenge, The latest Fair Credit scoring Operate (FCRA) distills the to exercise. You might dispute incorrect or incomplete guidance, including personal data, levels that do not fall into your, commission background or account stability which can be incorrect, or recommendations that is outdated.

Being aware what brought about an underwriter never to approve your loan can be make it easier to end a terrible benefit if you try once again which have a different sort of financial.

Examine FHA Pricing

Even though it is enticing to go it by yourself and you may work truly that have a seller, consider the feel an agent could offer to you while the a prospective homebuyer. You might control the experience towards a much better deal to you personally and your loved ones.

Different kinds of lenders include their guidelines that lenders and you can borrowers need go after. The principles and you can direction you to definitely apply to FHA mortgage brokers was requirements that You authorities put within the insurance coverage program.

When you’re entering the FHA loan application process as well as have come at your employment for less than 2 years, you have particular questions and also some misunderstandings that require fixing. You might have specific employment openings that need explaining.

Income and you will work verification because of the financial is necessary as an ingredient of process of bringing an FHA mortgage. This might have a look odd given that certain potential borrowers try retired, but there is a section of society that is to invest in the very first domestic while having receives old age earnings.

For those who have invested its entire mature lives once the renters, the latest homebuying processes will be overwhelming. Perhaps financial conditions try confusing, requirements for finding financing was unsure, otherwise down payment discounts merely aren’t offered. You will find a government-backed financial system designed for all of them.

While the most common FHA loan candidate has created some type regarding credit rating, certain individuals are only starting out. An effective borrower’s decision to not ever explore or present credit to determine a credit score may not be put due to the fact cause for rejecting the loan application.

FHA financing legislation state, “The minimum many years ‘s the decades where a home loan note are going to be lawfully implemented in the county, or any other jurisdiction, in which the property is located.” Its an extensively stored religion that there’s an optimum decades cutoff to possess recognized borrowers, most likely as the some people incorrectly envision FHA finance are merely to own first-time homebuyers.

FHA Loan Questions and you may Responses

FHA financing guidelines are designed to avoid the use of an enthusiastic FHA-funded home for what it phone call transient occupancy of a month or faster. That is why FHA money are not designed for bed and you may morning meal functions, condominium lodging, trips land, timeshares, etcetera.

FHA loan requests is actually analyzed having a number of factors of lenders direction. It isn’t always the scenario you to definitely a good borrower’s complete qualifies. Balances and precision of money form a number of it won’t amount as it from bucks for the bank.

The fresh FHA loan guidelines for selecting a multiple-equipment assets are located in HUD 4000.1, possibly known as the newest FHA Handbook. FHA loan regulations permit the acquisition of a home and no more than five way of living units, to the stipulation that borrower need live in among the fresh units.

To begin with, an enthusiastic FHA loan can not be regularly get a property you to was strictly commercial. if the home is categorized just like the mixed-explore and also at minimum 51% of one’s floors city can be used having home-based life, it is allowable.

Alternatives for people who happen to be having trouble repair their FHA funds appear. It is loan https://clickcashadvance.com/loans/loans-for-bad-credit/ mod, forbearance, and cost arrangements. The house Sensible Amendment Program (HAMP) is available previously to simply help individuals in big trouble, but not you to program has stopped being considering.

It may be much harder discover an FHA financing in the event the you might be mind-working, particularly if you are in the early degrees of your profession. Loan providers usually want to see an effective borrower’s money along the extremely latest 2 yrs. Huge field changes during those times may give them a reason to help you be afraid together with your financing recognition.